Our guide outlines whether the transfer of a business or part of a business should be treated as the transfer of a business as a going concern TOGC for UK VAT purposes and so outside the scope of UK VAT. It is important to be aware that the UK TOGC rules are mandatory and not optional.

Going Concern Linkedin

At the end of last weeks post we wondered whether BDOs large revenue gain would benefit employees during comp conversation time.

. By Going Concern News Desk Now that raises have been doled out at Deloitte next up is PwC. Going concern assumption 2. Debt and equity offerings.

Strategic cost cutting 1. We calculated the average raise percentage for each step up in rank or promotion where data was available ie A1-A2 A2-S1 S2-S3 etc. Some stakeholders may perceive that something that is clear and that provides a link with financial reporting aspects of going concern has been deleted and replaced by something that is more comprehensive but less concise and clear with specific reference to going concern.

Going Concern and Significant Uncertainties ca 55. The transfer of a business as a going concern relates to a transfer of the whole or an independent part of a business to a taxable person for the purposes of continuing the business that was transferred. Renegotiating existing arrangements 3.

Debt and equity offerings 2. 1 212-954-1723 KPMG explains how an entitys management performs a going concern assessment and makes appropriate disclosures. Going concern and financial reporting.

We welcome the initiative of the Financial Reporting Council FRC to set up the Panel to identify in the light of the credit crisis lessons for companies and auditors addressing going. Management intends to liquidate the entity cease trading or has no realistic alternative but to do so. Selling leasing or monetizing assets 4.

In certain circumstances an emphasis of matter paragraph may be added to a review report without affecting the auditors conclusion to highlight a matter that is included in a note to the interim financial information that more extensively discusses the matter. The educational material looks at four scenarios. As defined in GAAP substantial doubt about a companys ability to continue as a going concern exists when relevant conditions and events considered in the aggregate indicate that it is probable that the company will be unable to meet its obligations as they become due within one year after the date that the financial statements are issued.

Going concern and liquidity risks. Proposals to revise the guidance for directors of listed companies Timing of revised guidance PricewaterhouseCoopers LLP is a limited liability partnership registered in England with registered number OC303525. No material uncertainties 3.

There are special rules concerning properties and TOGCs. Significant doubts mitigating actions sufficient for going concern to be appropriate. The Standard defines going concern by explaining that financial statements are prepared on a going concern basis unless management either intends to liquidate the entity or to cease trading or has no realistic alternative but to do so.

The going concern basis of preparation is no longer appropriate. It assumes that the entity will continue to remain in business for the foreseeable future. Generally all goods and services that are necessary for the continuation of the business or part of it must be transferred to the transferee.

Material uncertainties remain 4. When preparing financial statements management shall make an assessment of the entitys ability to continue as a going concern. This is the first compensation cycle in the era of the New Equation which is just a fancy way for marketing purposes of saying that PwC has a client-first mentality and the firm likes to throw around the word trust many many News July 1 2022.

The registered office of PricewaterhouseCoopers LLP is 1 Embankment Place London WC2N 6RH. The IASB will be considering whether to add a project on going concern as part of its Agenda Consultation Any changes to requirements from these projects is some way into the future. In considering managements assessment of the entitys ability to continue as a going concern the practitioner shall cover the same period as that used by management to make its assessment as required by the applicable financial reporting framework or by law or regulation where a longer period is specified.

Conversely it also means that the entity does not plan to or expect to be forced to liquidate its assets. Significant doubts mitigating actions sufficient for going concern to be appropriate. We examined the 2022 2021 2020 and 2019 PwC comp threads on Reddit and the 2017 2016 2015 2014 and 2013 comp threads on Going Concern.

Further information about going concern is available in our InBrief and the COVID spotlight. Given all that has happened in 2020 and the continuing uncertainty in 2021 arising from the global pandemic we expect that investors are going to be looking at how companies and auditors are comfortable that a going concern basis of accounting is appropriate and the disclosures around it. Financial statements shall be prepared on a going concern basis unless management either intends to liquidate the entity or to cease trading or has no realistic alternative but to do so.

Going concern is one of the very fundamental principles of accounting. Katie Woods and Jamie Shannon discuss disclosures and judgements relating to material. MFRS 101 Presentationof Financial Statementspermits an entity that is no longer a going concern to prepare financial statements on a different basis but still in accordance with MFRS.

Potential actions that management could consider to help mitigate substantial doubt about the company continuing as a going concern include. Well the 2022 BDO. By Going Concern News Desk Last week we reported on BDO USAs stellar fiscal 2022 as the firm raked in just under 25 billion in revenuea nearly 25 increase over 2021s revenue of 2 billion.

To going concern in the audit. This document is intended to support the consistent application of requirements in IFRS Standards. Lessons for companies and auditors We appreciate the opportunity to respond to this review being undertaken by the Panel of Inquiry led by Lord Sharman.

A solution might be to retain this in the. QAs interpretive guidance and illustrative examples include insights into how continued economic uncertainty may. No significant doubts about going concern 2.

![]()

Pwc Archives Going Concern

Pwc Archives Going Concern

Going Concern Linkedin

Pwc Manager Believes Associates And Senior Associates Are Going The Way Of The Dodo Bird Going Concern

Pwc Archives Going Concern

Promotion Watch 22 The Queen S Pwc Adds 22 To The Partnership Going Concern

Going Concern Linkedin

Pwc Staff Hit Back At Alan Sugar Lazy Jibe

Pwc Archives Going Concern

Cy82zsbzoibygm

Pwc Uk Is Being Very Picky About Who They Hire Yes Even In This Market Going Concern

Compensation Watch 21 Pwc Employees Are Getting A 5 Bump In Pay Update Going Concern

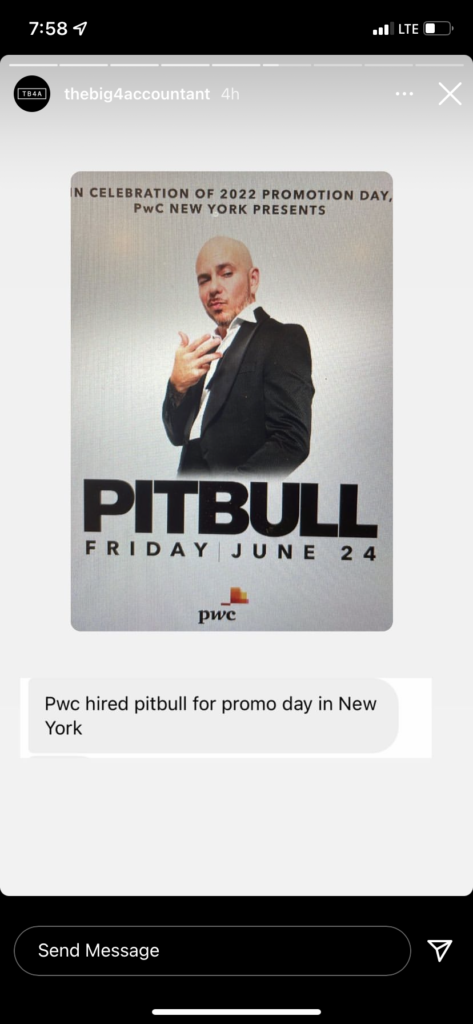

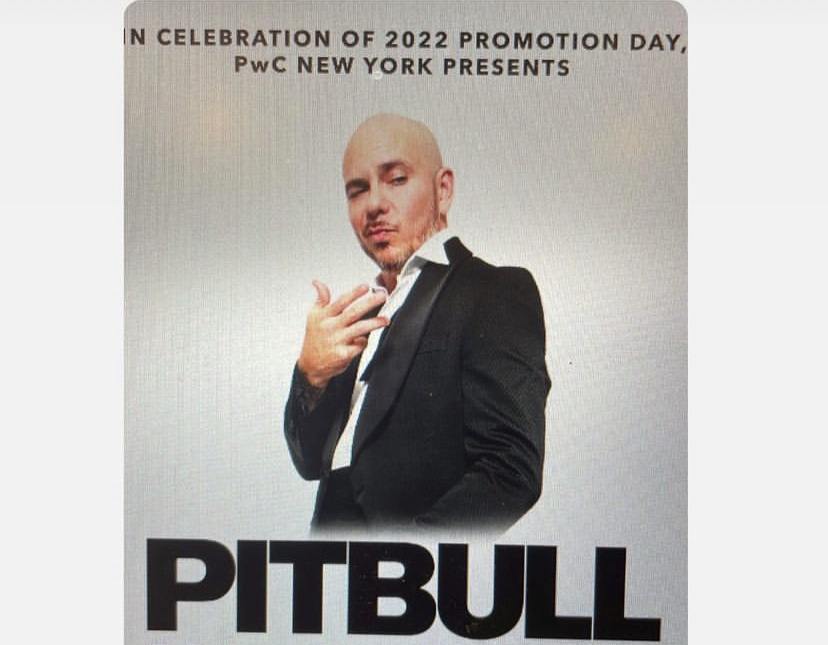

Updated Singer Pitbull Set To Perform His Worst Collaboration To Date Going Concern

Pwc Canada Is The Latest Big 4 Firm To Get Busted By Regulators For Employees Cheating On Internal Training Courses Going Concern

Updated Singer Pitbull Set To Perform His Worst Collaboration To Date Going Concern

Pwc S Uk Head Kevin Ellis Is Unhappy There Could Be Relief Going Concern

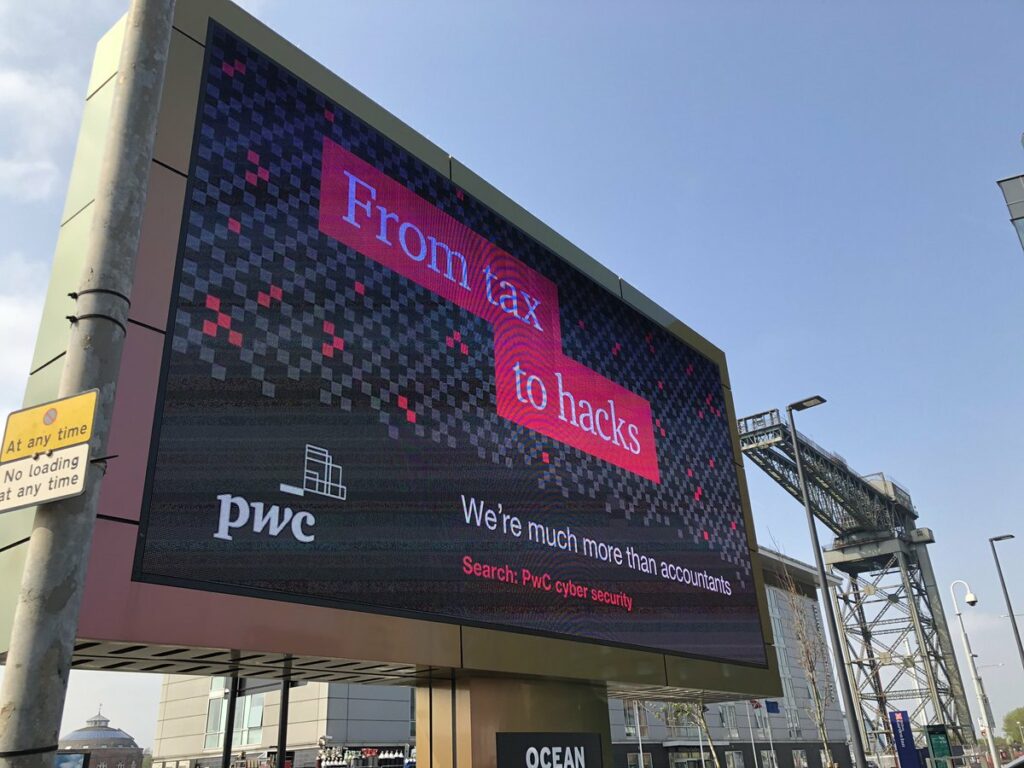

Pwc Is A Name You Can Trust Or So It Claims Going Concern

Kpmg Poaches Someone From Pwc And Issues A Press Release Part Xvi Going Concern

Pwc Archives Going Concern